European agri & food: 5 trends shaping 2023

Here is some food for thought. Agriculture has become a tricky dilemma. Although we definitely can not survive without it, we couldn’t absorb any more of the negative externalities it brings to a planet. In a way, we can say that agriculture is both the pain and the cure. It causes 20% of our country’s emissions but only weighs 2% of our GDP. It causes 75% of the world's deforestation but has the capacity to compensate for our global emissions (see Initiative 4 pour 1000).

This is where the notion of “regenerative agriculture” makes sense (cf our recent interview with Alice Legrix de La Salle). The notion implies that agriculture could be a net creator of biodiversity and play its role in terms of carbon capture while producing healthy products for humans.

However, this notion falls short when it comes to the social issues in agriculture. For instance, in France, more than half of French farmers are over 50 years old, which puts at risk our whole food system within a 10-years period (Plan de Transformation de l’Economie Francaise). Suicide is also twice more widespread as in any other job category (Le Monde).

That’s why I would say that truly sustainable agriculture should be characterized by the following five elements:

A soil capable of absorbing and stocking large water influx,

A soil capable of stocking a maximum of carbon,

An activity that is a net creator of biodiversity,

Feeding humans with healthy products,

Farmers under a sustainable living contract in terms of pay, social recognition, and living conditions - are willing to maintain our food safety.

This being said, it is clear that the path lying ahead is huge. But a good thing to realize is that agriculture and food have been one of the top 3 focuses of investors in 2022 - and will continue to do so in 2023.

Here is a snapshot of the top 5 subjects on which investors will focus their attention in 2023.

1. Derived alternative proteins: eggs, fish & co

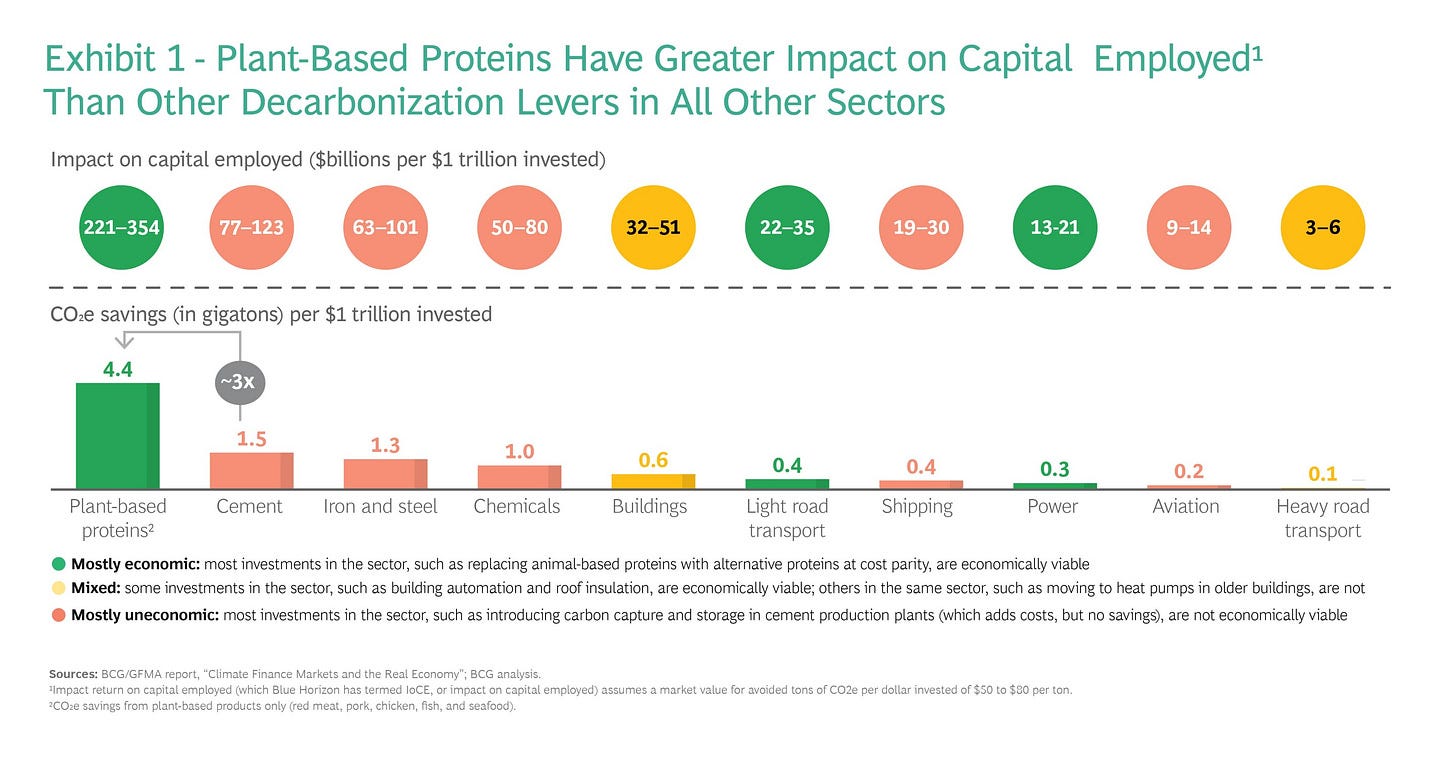

Alternative proteins have a unique role to play when it comes to climate change. By switching just 1 out of 10 meals to non-animal or “alternative” proteins, we can avoid as much carbon emissions as global aviation produces in an average year (Source: BCG x Blue Horizon)! As a consequence, the planetary “Impact on Capital Employed” (or “IoCE”) of alternative proteins (i.e. how much impact is created per dollar invested) is bigger than anywhere else.

People are making this transformation happen. In a BCG and Blue Horizon survey of 3,700 consumers around the globe, 76% said they were already familiar with alternative proteins. 76% said that a healthier diet is a primary motivator to try alternative proteins. 31% are motivated by climate impact but taste and price will be key to consumer adoption. 0% said they were willing to pay more for something as good without added value such as lower saturated fats or fewer antibiotics.

Meanwhile, production is scaling up to deliver lower prices and technology is advancing to deliver taste and health.

While plant-based meat alternatives are in their industrialization phase, cellular-based proteins (or hybrid) seem to be stuck in R&D and pre-industrialization, waiting for commercial authorizations (except in Singapore).

Meanwhile, companies in less mature alternative proteins have been thriving: from white meat (Upside Food) to fish (Current Foods, Wildtype), eggs, and milk (Remilk).

2. Weather & agricultural forecast

With climate change comes greater volatility in production volumes and timing, food shortages, and a relative incapacity of traditional weather forecast tools to adapt.

This context brings more and more operational and financial difficulties to all actors in the agri-food industry. Forecast is now vital to estimate the risk (and sell insurance policies) and anticipate future price evolution for negotiation purposes (for purchasing centers, retail companies, etc).

Companies in this field differ in:

The technology used: satellite-based (OneSoil) vs IoT-based (Trellis, Greenshield)

The degree of specialization: from pure weather forecasters selling to banks, insurers, event managers, etc. (HD Rain) to agricultural forecasters (Hyperplan)

In the US, there are already very mature companies that have succeeded in combining different yet highly complementary value propositions. For instance, Tomorrow.io is a listed company selling to a wide range of industries (big tech, airlines, car manufacturers, public institutions, etc.) with numerous weather intelligence services: platform, weather API, air quality monitoring, etc. This model is definitely virtuous from a market potential and resilience perspective. Spire is another example of how wide weather intelligence can go. Indeed, the company notably sells API solutions adapted to a specific industry.

3. Land monitoring & restoration

With the acceleration of extreme weather events comes more uncertainty regarding the evolution of “natural assets” (lands, forests, etc). This comes at a time when we finally realize how crucial they are — not only in terms of food safety — but also in terms of climate action. Indeed, forests absorb c.25% of our greenhouse emissions and reforestation has the power to bring us to carbon neutrality.

There are thus many use cases that legitimate tech-based land monitoring and restoration tools:

Selling carbon insetting/offsetting

Insure farmers or any other parametric insurance customer

As a consequence, several types of companies emerge:

Tech-based reforestation companies — such as MORFO (FR)

Land monitoring companies — such as Overstory (UK)

At this stage, it’s still hard to know what go-to-market will be the most successful. Either start by supporting farmers in carbon capture projects and then extend to biodiversity and land monitoring or launch a highly scalable solution relevant to a wide range of actors. The future will tell.

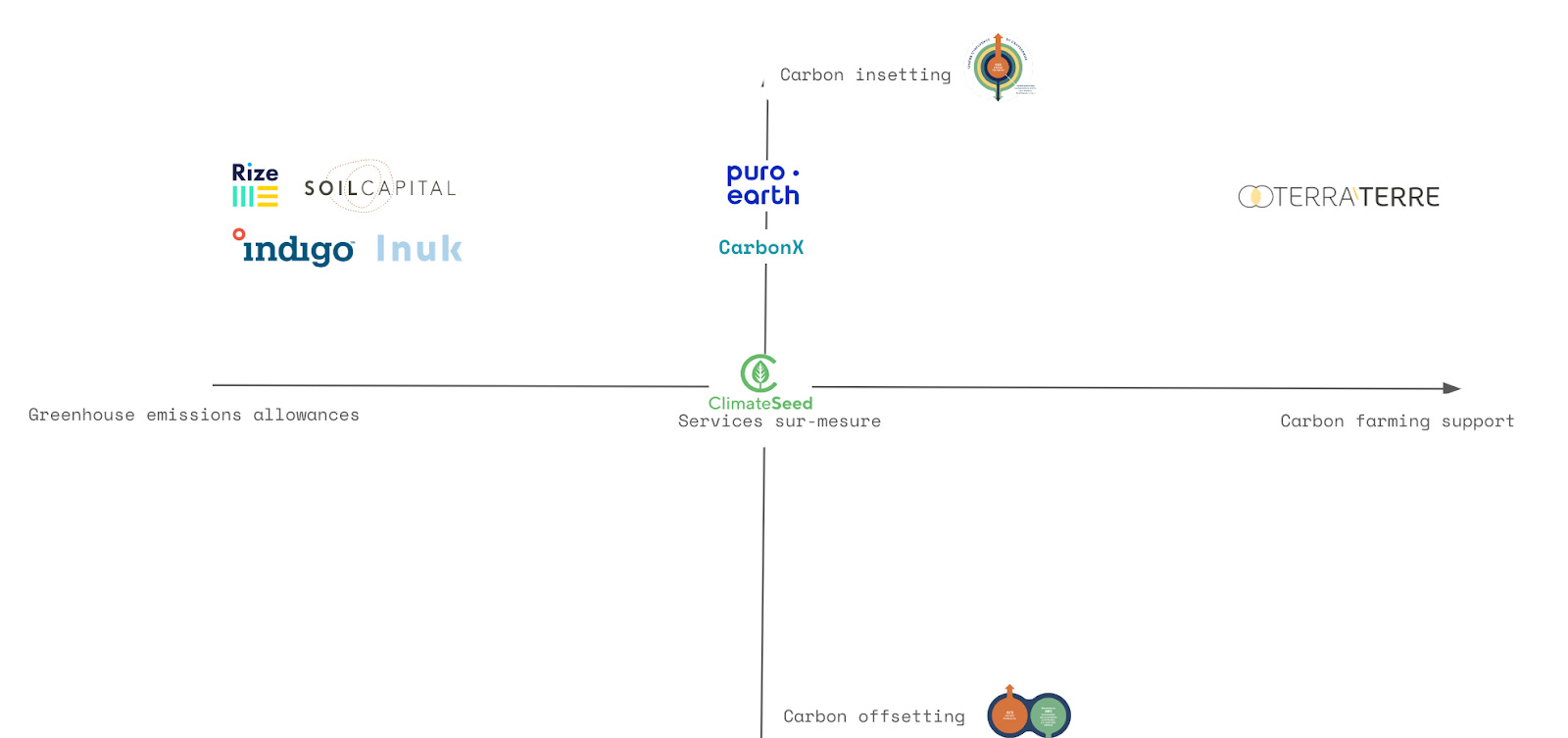

4. Commons incentivization

We are witnessing a massive awareness of the unique power of soil in terms of carbon capture (See Initiative 4 pour 1000). At the same time, we realize that the way we have conducted carbon offsetting has often been socially and scientifically uncomfortable: time gap and geographical gap between emissions and offset, quality gaps due to a lack of traceability and common standards…

There is a huge opportunity for companies that succeed in building a business model where farmers (or any other land owner) have incentives to create commons (i.e. positive externalities), where it would be carbon capture capacities but also biodiversity creation projects. In the carbon scope, some companies seem to address the challenges in a quite reasonable way: relocating carbon capture (97% happening outside of Europe) and linking directly buyer and seller.

Companies in commons incentivization differ in:

The lengths of perspective: carbon offsetting is a one-shot compensation action seen as a side project (e.g. typical tree planting) — where carbon insetting is a long-term capture action that is fully integrated into the value chain (recurring complementary revenue for farmers).

The removal technology: engineered carbon insetting (CarbonX (FR)) natural insetting (Terraterre, Soil Capital (BEL)). The latter method requires a certain level of intermediation with proprietary physical audits as there is no established trustee on this.

5. Anti-food waste facilitators

In 2008 the recession triggered Airbnb’s growth because budget restrictions “forced” the mass market to adapt to the new standard of peer-to-peer renting if they wanted to go on holidays. Today, it’s kind of the same situation — people accept more and more circularity in fields they never imagined of — because of budget constraints.

Anti-food waste companies have thus performed well this year — both in established models (Too Good to Go, Phenix) or in new models: B2C subscription to a basket of vegetables not meeting the standard retail specifications (Bene Bono - ex Hors Normes). There is a growing interest in the B2B business or anti-food-waste: mass catering for Too Good to Go, B2B “second market” for vegetables (Atypique, etc.).

Meanwhile, in the US, the market is already much more mature with several mega-rounds in “anti-food-waste facilitators”.

Do Good Foods - $170m

Misfits — $520m

Olio — $50m

Imperfect Foods — $120m

Those companies do not only bring digitalization to connect surplus to potential clients — but succeed in applying to food waste the same standard of the practicality of mass-market food players — such as home delivery.

The lesson from this last example may be that this topic might need to be dealt with from a bigger-picture point of view. Sometimes, adapting to mass market standards, if it is well done, means a bigger positive impact overall. For instance, La Poste has made huge progress on the environmental side of delivery. This should bring some hope seeds! 🌱

. . .

You are a digital health founder and you would like to reach out? Contact us at contact@ringcp.com or write to any member of the team on Linkedin. 📥